The post-banking-crisis era, paired with a prolonged higher-interest-rate environment, has permanently altered how corporations raise debt capital. For decades, commercial banks and public syndicated loan markets served as the undisputed gatekeepers of corporate finance.

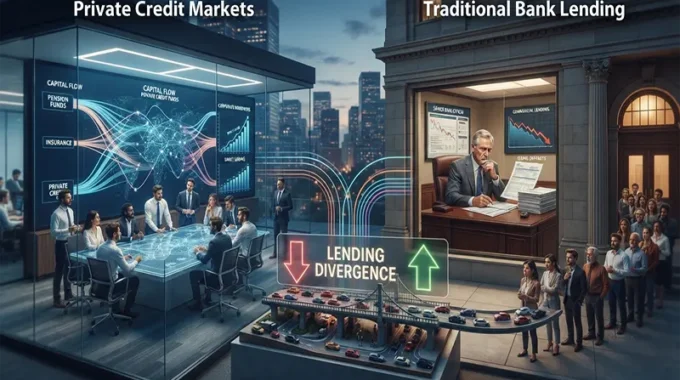

Today, that landscape is undergoing a massive structural shift. A tidal wave of corporate funding is migrating away from traditional banking institutions toward private credit and direct lending funds. As private debt asset pools swell into trillions of dollars, traditional bank lending is being squeezed, forcing commercial institutions to fundamentally rethink their underwriting models, syndication desks, and corporate banking relationships.

Macro Drivers Fueling the Private Credit Boom

The rapid expansion of private credit is not a temporary market aberration; it is driven by powerful macroeconomic and regulatory forces.

- Regulatory Squeeze on Commercial Banks: Following tighter post-crisis regulations (including Basel III and emerging Basel IV capital frameworks), holding corporate loans on bank balance sheets has become significantly more capital-intensive and costly. Banks are incentivized to offload risk rather than retain it.

- The Private Equity Engine: Private equity sponsors driving leveraged buyouts increasingly prefer private direct lenders. Unlike public syndications subject to market volatility, private credit funds offer speed, absolute certainty of execution, customized covenant structures, and confidentiality.

- Institutional Yield Demand: Institutional investors—such as pension funds, insurance companies, and endowments—seeking higher yields in an inflationary world have poured massive pools of capital into private debt asset classes, providing direct lenders with unprecedented dry powder.

The Impact on Traditional Commercial Bank Lending

As non-bank financial intermediaries capture lucrative middle-market and upper-middle-market loan originations, traditional commercial banks are facing profound structural displacement.

- Disintermediation of Core Lending: Private credit funds are routinely bypassing banks entirely, cutting out the middleman for corporate borrowers seeking term loans, mezzanine financing, and growth capital.

- Strategic Pivots by Banks: To defend their market share and maintain client relationships, major commercial banks are pivoting their strategies. Instead of holding loans, banks are partnering with private credit funds, providing “loan-on-loan” leverage financing to debt funds, or shifting toward fee-based advisory and underwriting roles.

- Shifting Risk Profiles: With private credit capturing higher-yielding corporate borrowers, traditional bank loan portfolios face potential concentration risks, often retaining lower-margin or more heavily regulated corporate clients.

Structural Risks and Liquidity Dynamics in Private Markets

While the growth of private credit has been celebrated as a triumph of financial innovation, the migration of debt outside the traditional banking perimeter introduces distinct systemic questions.

- Transparency and Valuations: Unlike publicly traded corporate bonds or syndicated loans with daily market pricing, private debt assets are illiquid and marked-to-model rather than marked-to-market. Valuing these portfolios during macroeconomic stress presents unique governance challenges.

- Covenant Erosion: In intensely competitive bidding environments among direct lenders, “covenant-lite” structures have occasionally surfaced, potentially weakening lender protections if corporate borrowers experience cash-flow crunches.

- Untested Credit Cycles: A significant portion of the private credit asset class scaled during an era of cheap money and economic expansion. A prolonged recession or credit downturn will serve as the first true stress test for many newer direct lending platforms.

The Future of Corporate Debt Capital

Private credit is no longer merely an alternative asset class; it is a permanent cornerstone of modern corporate finance, coexisting, competing, and increasingly collaborating with traditional commercial banking.

For corporate treasurers navigating this dual-track lending ecosystem, understanding the interplay between bank liquidity and private debt flexibility is essential for optimizing capital structures, managing refinancing risks, and securing resilient long-term funding.