Corporate Funding Migration to Private Credit Markets and the Impact on Traditional Bank Lending

The post-banking-crisis era, paired with a prolonged higher-interest-rate environment, has permanently altered how corporations raise debt capital. For decades, commercial banks and public syndicated loan markets served as the undisputed gatekeepers of corporate finance.

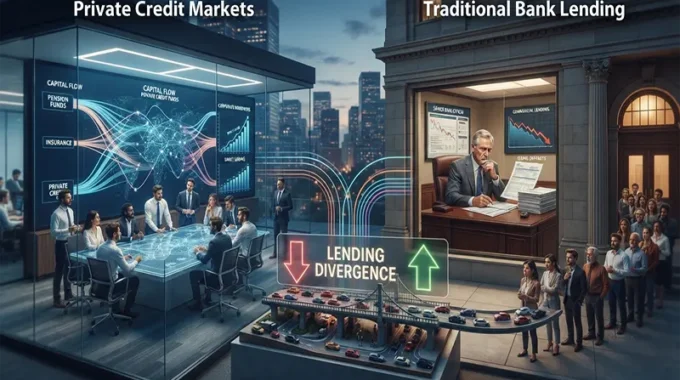

Today, that landscape is undergoing a massive structural shift. A tidal wave of corporate funding is migrating away from traditional banking institutions toward private credit and direct lending funds. As private debt asset pools swell into trillions of dollars, traditional bank lending is being squeezed, forcing commercial institutions to fundamentally rethink their underwriting models, syndication desks, and corporate banking relationships.

Macro Drivers Fueling the Private Credit Boom

The rapid expansion of private credit is not a temporary market aberration; it is driven by powerful macroeconomic and regulatory forces.

- Regulatory Squeeze on Commercial Banks: Following tighter post-crisis regulations (including Basel III and emerging Basel IV capital frameworks), holding corporate loans on bank balance sheets has become significantly